The 2026 FIFA World Cup kicks off at 8 pm on 11 June on the other side of the pond, opening with Mexico vs South Africa. But beyond the action on the pitch, there is another high-stakes tournament underway, the battle for your living room.

We know when football goes global, TV sales go into overdrive. During Euro 2024, retailers reported a 25% surge in sales versus an average month. Back in 2018, World Cup demand was so intense that it could have filled 10 football pitches with the TVs sold.

And 2026 is shaping up to be a record-breaker for the TV category.

With kick-offs landing at awkward hours, 5 am screamers and 11 pm deciders, some fans may be ditching the pub for their PJs. Betting giant William Hill predicts sales double that of 2018.

Sales of second screens, from small bedroom TVs to tablets, will also soar as people watch along in bed.

Which brands have the best form for the World Cup shoot out?

To answer that, we have taken a fresh look at the category using our Brand Divergence Index (BDI). BDI measures where brands sit across the axes of Differentiation and Attraction relative to their competitors. In football terms, it is a way of understanding who is genuinely playing a different game. The further a brand diverges from the pack, the stronger its correlation with purchase intent and value share growth.

Looking at the data from April 2025 versus March 2026, it is clear that brands have sensed the opportunity. In what looks like a pre-World Cup push, the entire category has stepped up. The baseline has lifted. Average BDI scores have risen. The playing field has become tougher.

But not all improvements are equal. Some brands have simply kept pace, while others have made more decisive moves.

The biggest shifts have come from Sky Glass, Toshiba, Philips and Panasonic. These brands have made plays bold enough to break out of their previous positions and into better territories.

Sky Glass is the brand dominating the conversation. By driving a sharp increase in Difference, it has pushed into the ‘Deviant’ challenger space. High levels of interest and sharing have been driven by its immersive campaign featuring Andrew Garfield, combined with expanded distribution across more than 200 Currys stores. Every touchpoint aligned towards one message – making the viewing experience feel more all-consuming. It has perfectly framed itself for the World Cup as the best way to experience major live moments. See a great write up of the campaign from Little Black Book here.

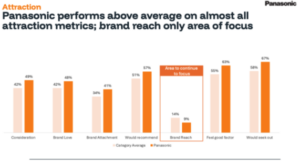

Panasonic, meanwhile, has taken an alternative approach to driving Difference. Rather than chasing attention through big campaigns, it has quietly built Difference through product, credibility and presence. Over the past six months, the brand has focused on expert validation, seeding reviews through trusted platforms like Which?, while strengthening its retail footprint.

It has launched a new 2026 European TV line-up, including OLED models like the Z95B and Z90B, alongside expanded Mini LED and large-screen ranges. Perfect for World Cup viewing from big screen to the bedroom. Panasonic has not shouted the loudest, but it has given people compelling reasons to choose. That has been enough to push it into the coveted Divergent space.

It still has room to grow Attraction further. Panasonic has built a winning system, but more people need to hear that story. This is one of the rare cases where increased media investment could genuinely amplify an already strong position.

Then there are Toshiba and Philips, both of which have focused less on standing apart and more on broadening their appeal. Both have successfully increased Attraction, moving themselves into consideration at a time when more consumers are entering the market. Crucially, they have done this by strengthening emotional connection. Positive associations are up. Brand attachment is building. These are not superficial gains; they are the foundations for valuable future growth.

Toshiba, in particular, has stepped up its presence with a more visible and outward-facing approach. Its “Seeing is Believing” platform has been brought to life through high-attention partnerships with the BBC and Marvel, including an integrated experiential campaign celebrating 60 years of Doctor Who. It is a smart use of a limited budget that we love. Leaning into cultural relevance and nostalgia to build emotional resonance rather than trying to outspend competitors.

What is striking across all four brands is that there’s no single playbook. Some are winning through scale and visibility, others through product and credibility, and others through emotional connection. But they all share one thing: they have made deliberate choices to move, not just maintain position. And in a tournament like this, standing still is the quickest way to fall behind.

The brands yet to break out: TCL and Lenovo

TCL and Lenovo show how easy it is to get stuck in the middle of a World Cup surge. Both brands have seen small lifts alongside the wider category, benefiting from increased visibility, retail presence and value‑led appeal, but they remain firmly in the Default space, below average on both Attraction and Difference.

What they are doing right is clear. Both brands compete hard on specification and price, showing up strongly in retail environments where screen size, resolution and promotional deals do the heavy lifting. This approach keeps them competitive when demand spikes, particularly for second screens or entry‑level upgrades. But the data suggests it isn’t translating into stronger emotional response, talkability or standout brand meaning, the things that most strongly drive Difference within BDI.

On a World Cup scale, that creates a ceiling. Without a clearer role in the category or a more distinctive reason to choose them, TCL and Lenovo are likely to benefit from increased sales without shifting how they are perceived. They are present, practical and good value, but in a moment dominated by brands selling the ultimate viewing experience, that can leave Default brands riding the wave rather than shaping it.

If you want to understand which brands are genuinely set up to win, not just ride the World Cup wave, our Brand Divergence Index can give you a clear read on where growth will come from, and where it will not.

Get in touch to see how your brand stacks up and identify the moves that will help you outsmart your competition.